International Women's Day: Insurance, a Topic of Equality?

Even in 2020, women own fewer insurance policies than men. Why?

Ten years ago, a survey on insurance gained a lot of traction. It showed that women own fewer insurance policies than men. We call this the gender insurance gap. There can be many reasons for this: Women are often co-insured with their partners or simply do not consider some insurance products to be relevant. In addition, women still get paid less; we know this as the gender pay gap. Since they have less money available, they invest less in insurance and retirement planning.

Gender Insurance Gap: women own fewer insurance policies

March 8 is International Women's Day and we are wondering: What about gender equality in insurance today? Are women sufficiently considered in insurance policies and what does digital insurance do to counter the gender insurance gap?

The data shows: It is important to sensitise women to the subject of insurance – there is still a big gap here. Breaking down barriers is therefore a major concern. Because one thing is clear: Our aim is to provide men and women alike with insurance policies – and in doing so, offer them more security.

Women have less insurance, are often co-insured and less willing to take risks

As of today, Getsafe has 37% female and 63% male customers, which is already a remarkable number. Amongst under 25-year-olds, 44% of customers are female. Of customers under 30, 41% are female. This is a significant trend which shows that digital insurance is narrowing down the gender insurance gap. Let's take a closer look.

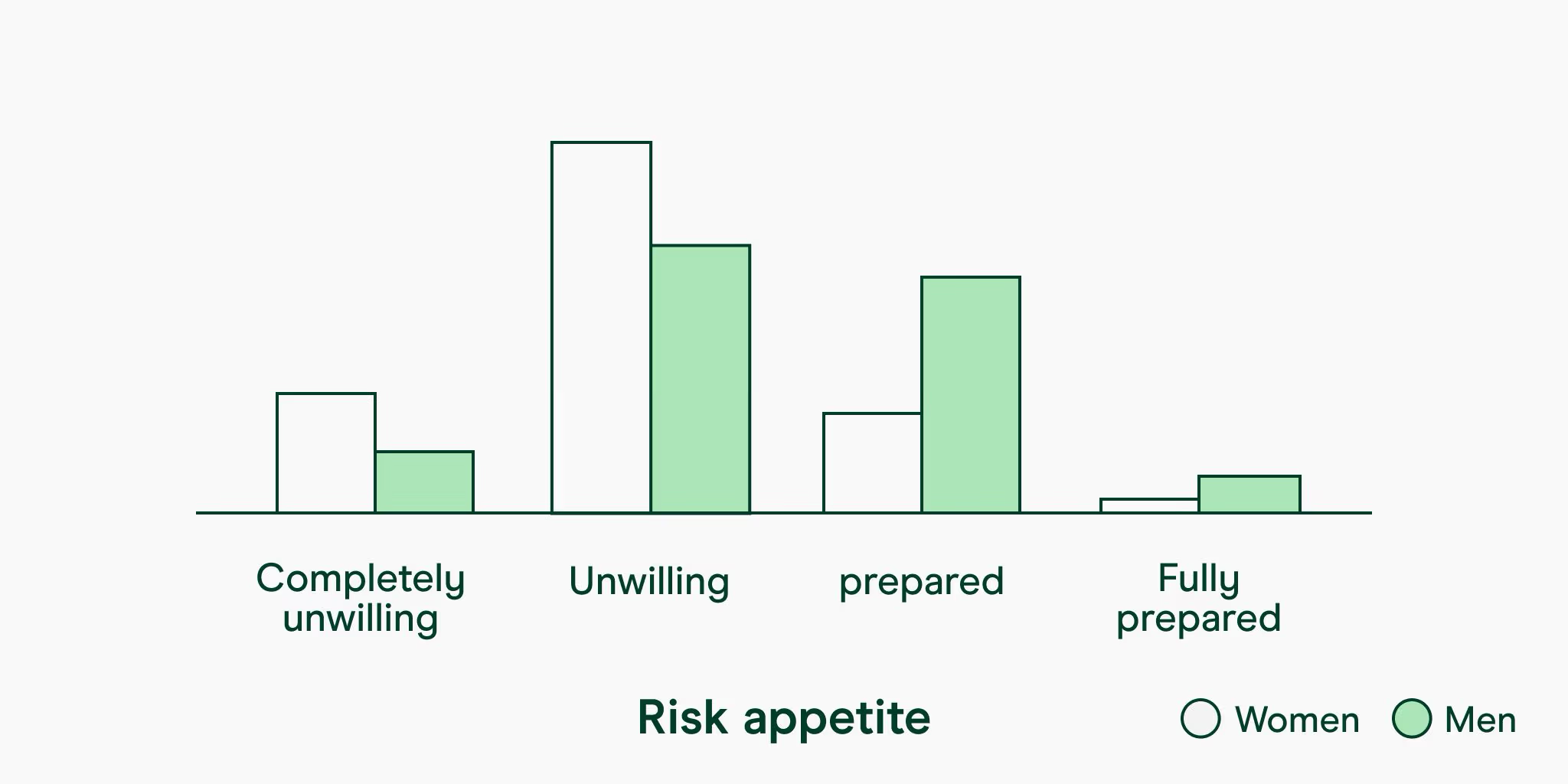

When using our app, our members do a short personal assessment that helps us better understand who they are and where they stand in life. One question is about their attitude towards risk. The results show that female customers consider themselves to be significantly less willing to take risks than our male customers.

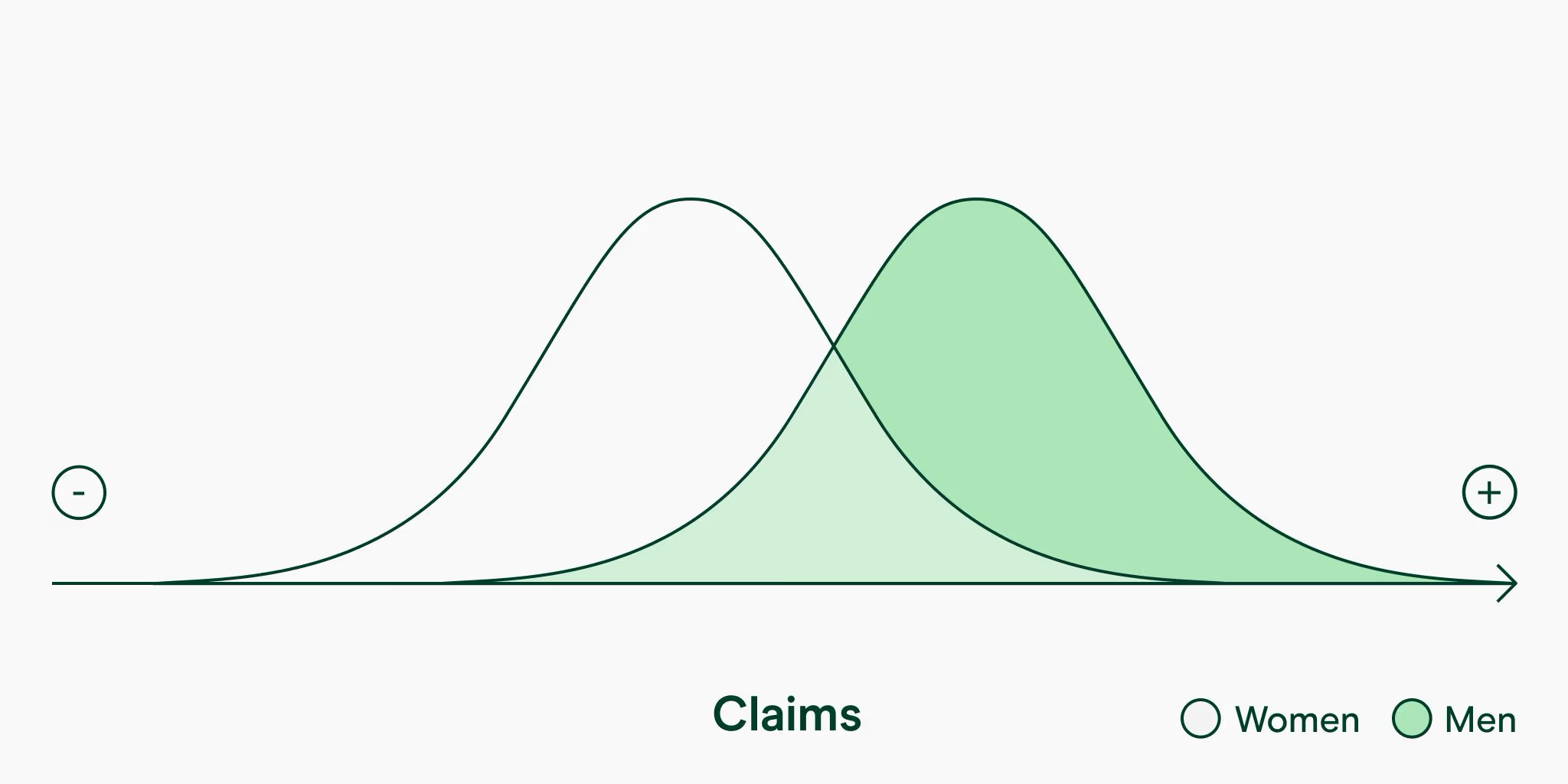

Not only are women more risk averse, they are also less likely to claim.

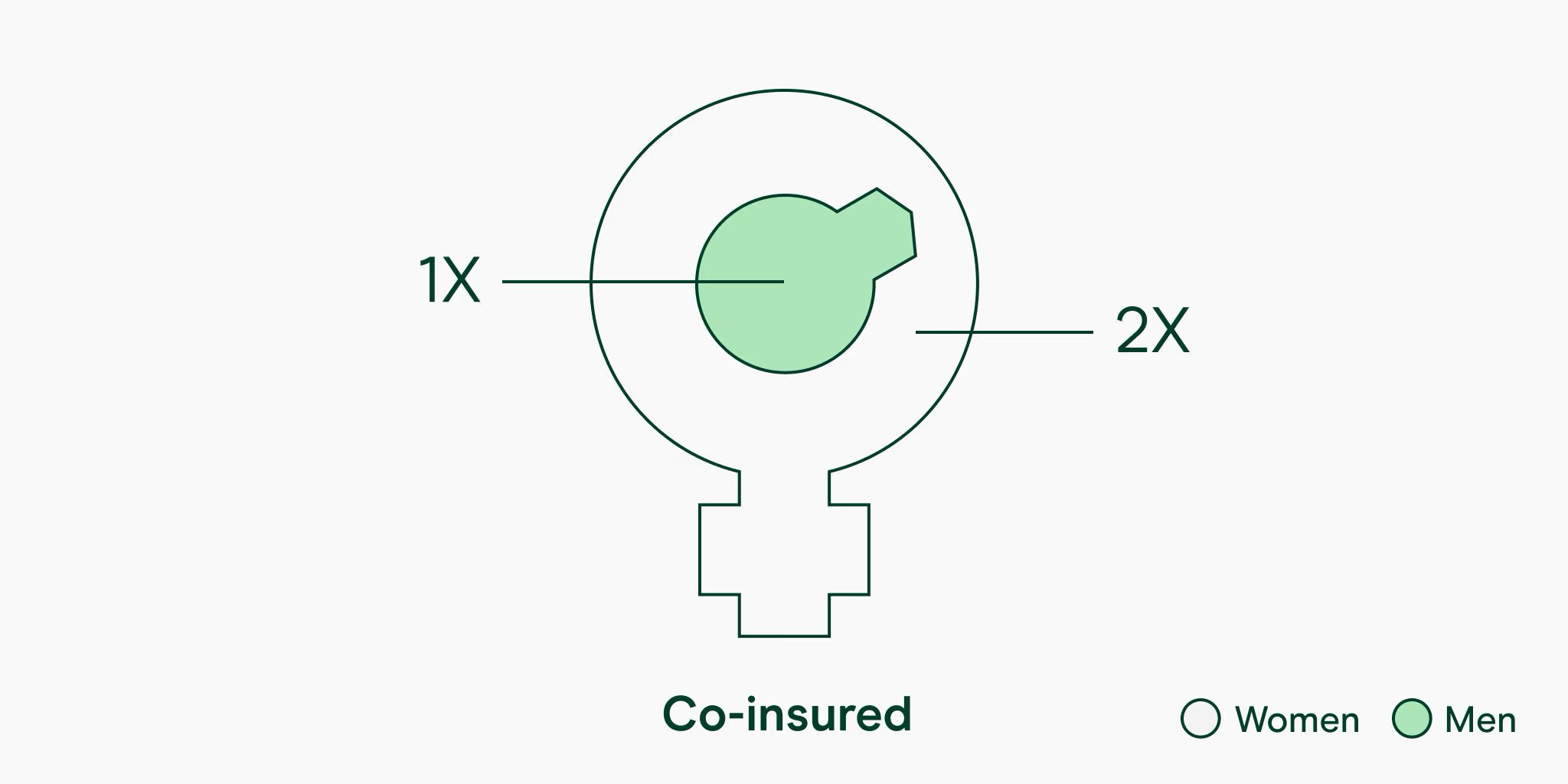

Taking a closer look at our Policy Networks feature, we see that twice as many women are listed as the co-insured person compared to men, for example in products such as liability or contents insurance.

One thing that really strikes us is the fact that male customers are twice as likely to buy legal insurance as female customers. How is this possible, considering that, even today, many women still face difficulties in their professional environment, for example when it comes to pregnancy and maternity leave?

In addition, for a long time women paid more for insurance, for example for occupational disability or health insurance. Following a ruling by the European Court of Justice in 2011, unisex tariffs have become mandatory, which means that insurance companies are no longer allowed to differentiate according to gender. What many do not know: insurers have not automatically adjusted their policies prior to 2012. Women affected should consider switching to a unisex tariff, as this is often cheaper.

What we do – digital insurance as key

We approach this topic through a fair price, transparent communication and an intuitive user experience. A few examples:

The getsafe app is very intuitively built and easy to understand. What is insured – and what is not? What protection do I have – what do I need? We only make products that we ourselves consider sensible. Also, insurances can be cancelled on a daily basis, claims can be submitted 24 hours/7 days a week via the app.

Our tool Policy Networks gives co-insured persons access to the Getsafe App. This means that policyholders can add them via the app, thus making many of the app's benefits available to them – co-insured persons can see exactly where they are insured, what is covered and what is not, or download important documents such as the insurance policy. For us, this is an important element on the way to picking up all policyholders and educating and empowering them in dealing with their insurance coverage.

As a technology company our work is based on data. Evaluating it enables us to offer a holistic and positive user experience and to draw the attention of our policyholders to gaps in their insurance coverage. We can evaluate policyholder data across lines of business and thus carry out a holistic analysis of our users’ needs. With tools such as our needs check, we get to know our policyholders better and better. We know what they’re currently up to and can make offers based on their needs and habits.

We are already on a good path – but there is still a lot ahead of us. We will continue until we have reached our goal. Let us know if you have any ideas on how we can improve. We are looking forward to the exchange with you!

What might also interest you: "Women and insurance – a long way to go?"